The Cost of Capital is defined as the rate of return that a company must offer on its securities in order to maintain its market value. Financial managers must know the cost of capital in order to (a). make capital budgeting decisions, (b). help establish the optimal capital structure and (c). make decisions concerning leasing, bond refunding and working capital management. The cost of capital is computed as a weighted average of the various capital components, items on the right hand side of the balance sheet such as debt, preferred stock, common stock and retained earnings.

Understanding the Cost of Capital

WACC – Cost of Capital

Each element of capital has a component cost that is identified by the following:

ki = before tax cost of debt

k¬d = ki (1-t) = after tax cost of debt, where t = tax rate

kp = cost of preferred stock

ks = cost of retained earnings (or internal equity)

ke = cost of external equity, or cost of issuing new common stock

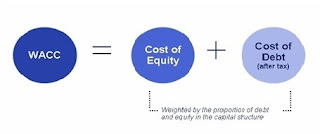

ko = company’s overall cost of capital , or a weighted average cost of capital

The after tax weighted average cost of capital (WACC) is given by the following formula: WACC = ka = ke = (S/V) + kd (1-t) (D/V)

Cost of Capital

Suppose this firm faces a corporate tax rate of 40%, has variable expenses equal to 30% of sales, and has fixed costs of $158.

Working back from these requirements we can forecast the level of sales the firm must earn in order to achieve these operating results…thereby setting a sales performance target for management.

Working backwards, we get:

Sales = X

Variable Costs = .3X

Fixed Costs = 158

EBIT

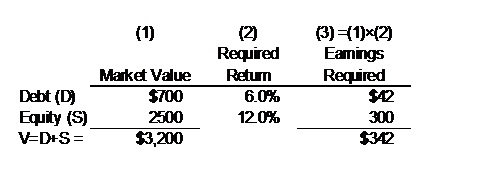

Interest = 42

Taxes (40%)

Net Income = 300If sales = X, then VC = .3X and X – .3X – 158 = EBIT

(EBIT – I)(1-T) = NI so (EBIT – 42)(1-.4) = 300 => EBIT = 542 which => X = 1000, and so VC = 300 and also Taxes = (542-42)(.4) = 200, so:Sales = 1000

Variable costs = 300

Fixed costs = 158

EBIT = 542

Interest = 42

Taxes (40%) = 200

Net Income = 300This working backwards process is the approach taken by regulators to set pricing for rate of return regulated industries, like utilities. So cost of capital drives utility rate increases!

Assuming earnings are a perpetuity, we have: Perpetuity – Cost of Capital

Firm ABC has:

Debt D of 8% annual coupon bonds with 10 years to maturity and book value of $1 m.

Preferred shares P with 10% annual dividend and book value of $1 m.

100,000 Common shares originally issued at $15/share for a value of $1.5 m.

Retained earnings of $0.5

Total of $4 m.

Market values:

The present market rate of similar risk 10 year bonds is 6% so the market value of the bonds is given by 80,000PVIFA(10 years, 6%) = [80000/.06](1-1/1.06^10) + 1,000,000/1.06^10 = $1,147,202.

Similar risk preferred shares are providing yields of 8%, so the market value of the preferred shares is 100,000/.08 = $1,250,000.

The market value of the common shares is currently $25/share, so the total market value of the shares is $2,500,000.

The market value of the firm’s balance sheet V = D + P + SE = $1,147,202 + $1,250,000 + $2,500,000 = $4,897,202 and D/V = .234, P/V = .255 and SE/V = .511.At HelpWithAssignment.com we provide best quality Assignment help, Homework help, Online Tutoring and Thesis and Dissertation help as well. For any of the above services you can contact us at https://www.helpwithassignment.com/ and https://www.helpwithassignment.com/finance-assignment-help