- Home

- About Us

- Services

- Online Assignment Help

- Auditing Assignment Help Service

- Nursing Assignment Help

- Excel Assignment Help

- Advanced Economics Homework Help

- XML Assignment Help

- Strategic Management Assignment Help

- Logarithm Assignment Help

- Probability Assignment Help

- Matrices Assignment Help

- Commercial Bank Management

- Thesis Proposal Help

- Corporate Strategy

- Electrical Engineering

- Civil engineering

- Mechanical Engineering

- Electronics Engineering

- Financial Plan Development

- Research Paper

- Political Science Assignment Help

- Operations Management Assignment Help

- Computer Vision Assignment Help

- Commercial Bank Management

- IT Security Assignment Help

- College Essay Help

- Term Paper Help

- Medical Science Assignment Help

- Nursing Thesis Writing Help

- Religion

- Thesis Help

- Supply Chain Management Assignment Help

- Australia Assignment Help

- Cause and Effect Essay

- International Finance Assignment Help

- Statistics Assignment Help

- Computer Science

- Information Technology

- Bioinformatics Assignment Help

- Biostatistics Assignment Help

- Excel Assignment Help

- Taxation

- Research Proposal Help

- SAASU Assignment Help

- Auditing Assignment Help Service

- Workplace Learning in Finance

- Dissertation & Homework Help

- Custom Essay Writing Help

- Online Assignment Help

- Reviews

- Tutors

Publish On: September 11, 2012

By HelpWithAssignment

Learn Weighted Average Cost of Capital (WACC)

-

Conquer Deadlines with Expert Help

-

1M+ Happy Students

-

11+yr Legacy

Rated #1

Provider for the last 10 successive years

99109+

Assignments delivered. 543 + , just today

The Weighted Average Cost of Capital (WACC)

It is rare to find a company relying solely on one source of funds. The balance sheets of even modest-sized businesses show that companies raise investment funds through a variety of channels. Furthermore, they pay different rates on the various components of their capital structures. The resulting overall cost of capital, is usually referred to as the weighted average cost of capital (WACC). As the term suggests, the WACC is simply the sum of the costs of the individual components of capital where each component is weighted in accordance with its relative importance in the total capital structure.

The WACC is important for two closely inter-linked reasons:

- The analysis of the cost of the individual components of capital showed that the cost of capital is pivotal to the relationship between expected future cash flows accruing to a particular capital asset and the market value of the asset. We saw that the market value of a capital asset is the discounted value of the expected future cash flows, with the cost of capital acting as the discount factor. Similarly, a company’s WACC is critical to measuring the relationship between the expected future cash flows and the total market value of the company.

- The analysis of the WACC allows us to confront the question of whether changes in the level of gearing can affect the overall cost of capital that a company pays and, by implication, the total market value of the company’s assets. In other words, does there exist an optimal capital structure, where the cost of capital is minimised and the value of the company maximised?

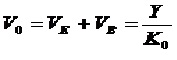

Assume that a company’s capital structure consists of two components: equity and irredeemable debt securities (the assumption of irredeemable debt makes the initial demonstration of the key points easier). Furthermore, assume that the company generates a constant annual net cash flow, which is paid out in full as dividends and interest. This means that:

where: V0 = total value of the firm

VE = market value of equity

VB = market value of debt

Y = net earnings

K0 = weighted average cost of capital

This merely states that the current value of the firm is the sum of the market value of its equity capital and the market value of its debt capital. This, in turn, is equal to the discounted value of its net earnings, where the discount factor is the WACC. The latter point should not be difficult to grasp. If the market value of equity capital is the expected dividend cash flows discounted by the cost of equity, and the value of debt is the expected interest payments discounted by the cost of debt, then the total value of the firm will be the total net earnings discounted by the WACC. Hence, a simple manipulation of the above equation means that:

where: KE = cost of equity

KB = cost of debt

Therefore:

And:

And:

where: D = total dividend payment

I = total interest payment

Therefore:

It is clear from these formal equalities that an alteration in the level of gearing will only affect the company’s market value if it causes:

- A change in the net earnings on the company’s operations

- A change in the WACC.

The first possibility can be easily dismissed. The net earnings depend solely upon the use of the assets that the company has purchased. The way in which the purchase of the assets is financed is immaterial to the determination of the net earnings arising from their use. Changes in gearing will merely alter the distribution of the prevailing earnings among shareholders and bondholders.

The second possibility, of modifying the market value of a company through altering the level of in gearing, requires a more considered examination. Remember that the WACC is simply the flip side of the weighted average return expected by the investors in a company, which itself reflects the degree of systematic risk associated with the company’s operations. If a company replaces equity with (cheaper) debt, it increases the level of financial gearing. This means that the shareholders face more financial risk, leading them to demand a higher return. Hence the cost of equity rises, thereby neutralising the positive effects of increased debt finance on the WACC. The implications of a change in gearing on the cost of equity can be shown as follow

If:

Then:

Therefore:

Substitute ![]() for Y. Hence:

for Y. Hence:

i.e.

The latter formulation demonstrates that an increase in gearing (i.e., in VB/VE) must lead to an increase in the cost of equity capital. This suggests that there is no automatic benefit, in the form of a lower WACC, to the company arising from alterations in the level of gearing. The basis for this argument is that shareholders will demand compensation for the increased financial risk. Hence, there is no reason why investors, as a whole, should demand a different averagerate of return just because a company modifies the way in which it finances its operations.

For more details you can visit our website at https://www.helpwithassignment.com/finance-assignment-help and http://www.helpwiththesis.com.